Unlock a Housing Boom through Depreciation Bonuses

How Financial Frictions are holding back Housing and Taxes can Help

The mere mention of depreciation often sends people into a daze, conjuring images of labyrinthine tax regulations best left to the realm of accountants and those enthralled by fiscal minutiae. I want to convince you that the way we approach investment taxes is not just a dull financial chore — it's a pivotal battlefield in our quest to tackle the housing crisis. So let’s unravel how these seemingly esoteric tax principles could be the secret weapon we've been overlooking in the fight for housing affordability.

The 1980s CRE Boom

The 1970s and 1980s were an interesting time. As I’ve talked about here previously — this was the era of stagflation: shocks to financial constraints and the supply side of the economy which hit production in various ways. Modern treatments of monetary policy over this period think of this as a time of Fed overstimulating the demand side, but more recent work confirms that the supply side was a big part of the story as well.

The graph illustrates housing production trends, with multifamily production highlighted in blue. It's crucial to understand these trends in the context of economic fluctuations. The economy experienced recessions due to tightening financial conditions, which severely impacted housing production. This impact is visible in the inverse relationship between housing production and interest rates, represented by the 10-year Treasury rate shown in red. When housing production declined, rents (indicated in green) would increase, eventually leading to a resurgence in housing construction as economic conditions stabilized. High demand for housing, driven by the desire to invest in tangible assets as a hedge against inflation, also fuels this cycle of booms and busts in the housing market.

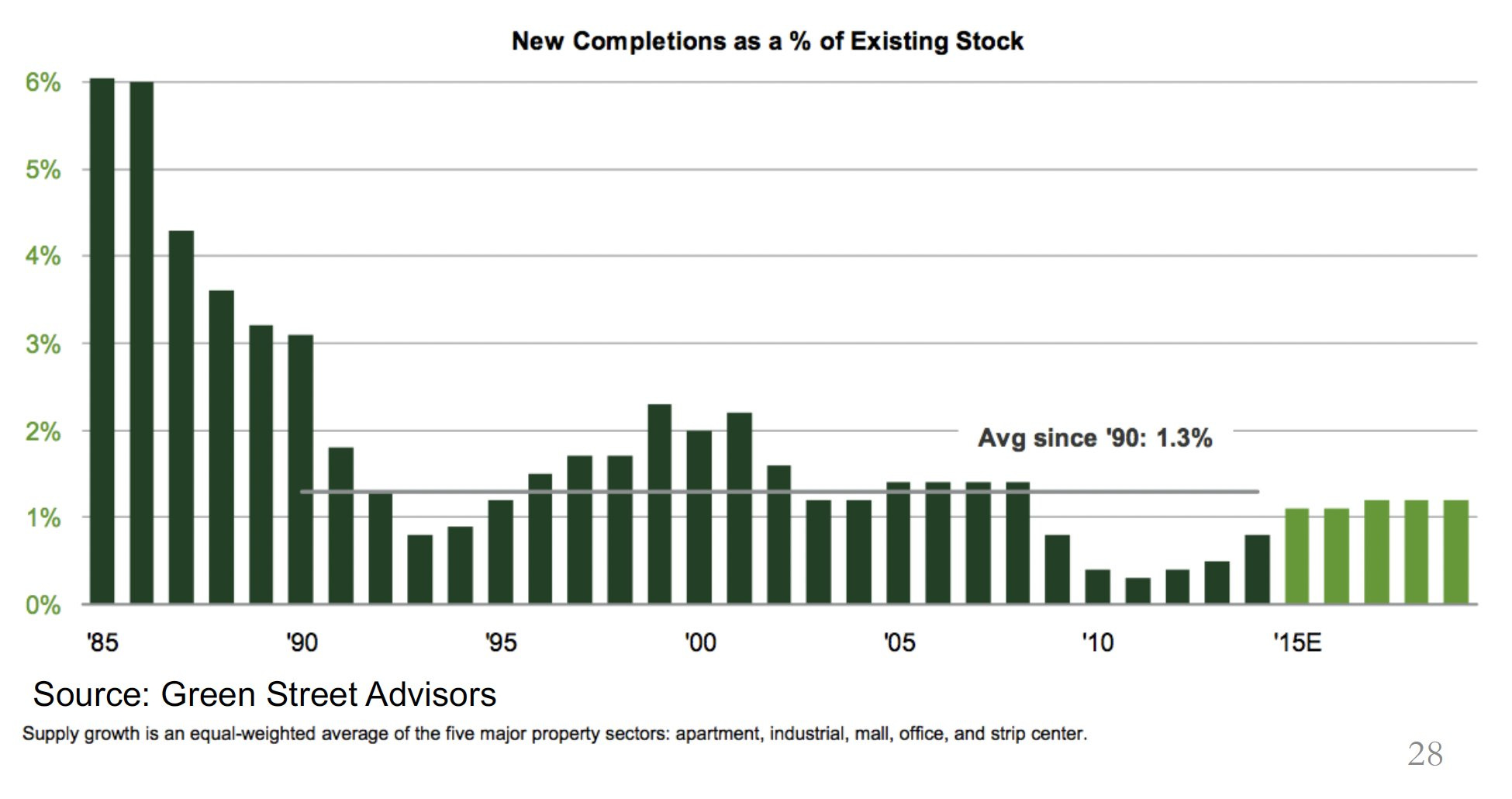

That was the macro backdrop heading into the 1980s: when interest rates continued to stay elevated (the 10-year Treasury averaged over 10% in the decade, with mortgage rates of course being above this). Based on everything I mentioned before, you would expect to see multifamily housing production would crater over this period given those high financing costs. After all, today we are also seeing declines in multifamily housing production even at far lower interest rates.

Instead, the 1980s were a booming decade for commercial real estate. We were producing more multifamily units in the early 1980s than even the post-pandemic apartment boom in absolute terms (even setting aside the fact that the population is a lot higher now). Commercial real estate, overall, you can see was growing as rapidly as 6% each year based on the size of the existing stock — a huge contrast to the construction in subsequent decades, especially the post-GFC bust.

So what happened? How did we boost commercial real estate production, especially in apartments, despite the high financing costs?

1981-1986 — Tax Depreciation Comes and Goes

This answer to this question comes in a great piece by Alex Muresianu who covers the impact of the 1981 and 1986 tax law changes on the depreciation of commercial real estate. The general idea is that when companies make investments in commercial real estate assets, they can write down the value loss or depreciation in the asset over time, recognizing these as a non-cash expense lowering taxable income, thereby increasing the after-tax returns for investment and encouraging firms to do more of it.

Just as important is the timing of when depreciation credits arrive. With accelerated depreciation, firms are able to write down more of the value of an investment earlier. Note that accelerating depreciation doesn’t change the total undiscounted amount of corporate tax receipts — but it means they arrive to firms much sooner to the time they make their investment.

Tax reform in 1981 had two big changes — it really lowered depreciation timelines from 36 to 15 years, and it increased the speed of depreciation from a 150% declining balance to 175%. This was a massive shock to depreciation schedules, and effectively brought forward heavily the tax benefit firms get from investing in Commercial Real Estate. The 1980s CRE boom in construction was the consequence.

Why does the timing of tax credits matter so much to firms? A great deal of corporate finance research has emphasized the importance of hurdle rates for investment: firms have fairly static rate of return requirements to engage in investment. Bringing forward the timing of tax benefits, even when it does not change the total tax liability paid over the life on an investment, raises the rate of return and can help projects pencil out. These are particularly important in real estate, given the large capital tangibility of the projects and financial constraints faced by developers. This is important enough that public housing advocates emphasize that using public funds for social housing can help projects which wouldn’t get funded by private developers employing high hurdle rates.

The 1980s CRE boom fizzled out by 1986, when the Tax Reform Act of 1986 (TRA86) again shifted depreciation schedules. While this tax reform package was good in many other dimensions (equating the highest end income and capital gains tax rates for instance), it turned out to be a disaster for real estate, by drastically extending depreciation schedules, which are now 39 years for commercial real estate (along with straight-line depreciation). The upshot is that developers experience drastically delayed cost recovery schedules for CRE investments. Inflation and the standard time value of money imapct lowers actual recovery rates further. Slowed development pipelines are the consequence.

The negative impacts of TRA86 were recognized immediately by commentators — James Poterba has an NBER paper from 1992 arguing “TRA86 reduced incentives for rental housing investment, contributing to the decline in new multifamily housing starts from 500,000 per year in 1985 to less than 150,000 in 1991. In the long-run these policies will lead to higher rents.” So the idea that housing affordability is impacted by the financing environment for builders isn’t new.

Now, there are a few other details I’m skipping over here. For one, many commentators have grown to think of tax rule changes as contributing to an “overbuilding” problem in CRE, especially as it was followed by financial distress in the asset class and the S&L crisis over this period. These were also related to other tax dodge issues in real estate, covered in Alex’s piece. There’s a lot more that can be said here, but suffice to say that it’s possible to boost the investment in CRE without adding additional tax haven benefits, and sitting here in 2024, with super high apartment rents, we have a different perspective on the problem of “overbuilding.”

TCJA in 2017

This brings us to another major revamp of the tax code — TCJA in 2017. This alleviated some of the tax code’s bias against investments, especially short-term investments. There was a broader debate over the tax bill passage over whether we should move to full expensing of all capital investments. The Tax Foundation estimates suggested that real estate would bear a large brunt of those tax changes, given how important long-lived structures are, and drive the largest increase in economic output.

As Paul Williams points out, the real estate industry itself opposed some of these changes:

The industry concerns with expensing are based on historical experience. Accelerated depreciation of real estate in the early 1980s led to tax driven, uneconomic investment. Tax-motivated stimulation of real estate construction that is ungrounded in sound economic fundamentals, such as rental income and property appreciation expectations, creates imbalances and instability in real estate markets. No other major country in the world has immediate expensing of real estate. The market implications of expensing real estate are risky, untested, and unpredictable. The negative consequences could harm state and local communities (through reductions in state and local property tax revenue), the financial security of retirees (through pension investments tied to real estate), and the banking system (through the declining value of real estate on bank balance sheets and systemic risk to the financial system).

In fairness to the industry — the real estate boom and bust cycles in previous decades were real, and you can obviously understand how increasing real estate production might shock rents. I’m not the first person to point this out, but it really is striking how NIMBYs are so skeptical of the link between lower increased supply and lower rents, in contrast to capitalists who see that link as crystal clear.

But just because real estate lobbyists don’t want more competition is not a good reason to give it to them. It’s important to fight against the real estate lobby and insist they receive tax benefits — that’s the best way to get new construction.

What Should Depreciation Schedules Look Like?

These accounting details are important in the context of development pipelines dry up across the country. Firms are looking at a weak rental picture in the next year or so, as the supply that was started during the pandemic comes online. But we’re facing the prospect of higher rents in the subsequent years — as the lack of construction today will ultimately result in a supply crunch and raise apartment rents in the longer term. But construction firms aren’t able to look this far forward and plan for more construction today, at least in part because of financing frictions, driven by higher interest rates and slower bank credit, which are shutting down plans for construction today.

One way to think about this shock is in terms of crowd-out. As federal spending has grown on projects like manufacturing through the IRA, interest rates have gone up and this has crowded out housing production.

A possible way to address the situation would be lowering interest rates through monetary policy, and there probably is some scope for that as inflation has come back down.

But accounting changes can also play a role. I think the optimal policy here would at least resemble the tax reform bill of 1981 — shorten depreciation schedules for commercial real estate and include bonus depreciation, so as to shorten investment cost recovery timelines and encourage a boom in construction. I also think the political economy for such changes might be more favorable than in the low interest rate environment of 2017. Back in 1981, we were looking at an environment with falling inflation but interest rates that remained stubbornly high, just as today. There is probably a greater willingness to consider changes in depreciation schedules in the context of addressing those financing frictions.

Even better would be full expensing — allowing firms to deduct the full cost of structures the year they incur the expense, the same way that is allowed with wages. The Tax Foundation estimates this would raise output by 2.8%, wages by 2.4%, and add 569,000 jobs. On top of that, it would likely reignite a multifamily housing construction boom which would bring down rents across the country.

It’s commonplace these days for YIMBYs to think about regulatory constraints — zoning and building codes — which hold back housing construction. I think increasingly they also think about operational costs for multifamily building operators which raise the cost structure and rents. Financing and accounting adjustments also need to be part of the pro-housing coalition agenda. The coming expiration of the TCJA by the end of 2025 is a good motivation to kick off the debate over how to structure the tax code to best support American prosperity.